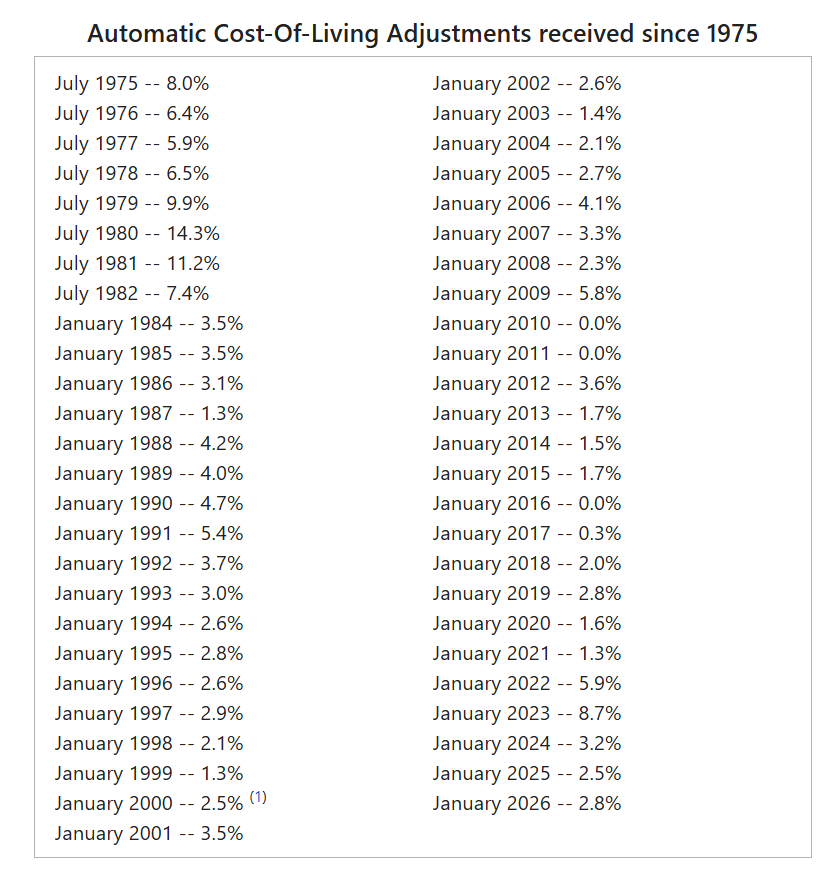

Although to some of us it may seem as if Social Security has always been around, that isn’t the case. The Social Security Act was signed into law by President Franklin D. Roosevelt on August 14, 1935. Its aim was to address the economic hardships of the Great Depression and provide an income source, specifically for the elderly. But automatic cost-of-living adjustments weren’t a part of the beginning stages. Prior to 1975, Congress had to enact special legislation to increase Social Security benefits. However, soaring inflation in the 1970s led Congress to allow automatic Social Security adjustments, tying them to the Consumer Price Index (CPI-W) to keep pace with inflation’s eroding effects. Congress enacted the Cost-of-Living Adjustment (COLA) provision as part of the 1972 Social Security Amendments, and in 1975, the first automatic Social Security COLA went into effect.

Highs and Lows

That first automatic COLA was one of the higher ones in the COLA’s history. At 8%, Congress was trying to fight against an inflation rate that doubled to more than 12 percent from 1969 to 1974. But this wasn’t the highest COLA on record. That belongs to the year 1980, with a whopping 14.3 percent, followed by the second highest at 11.2 percent the following year in 1981 as a result of what is known as The Great Inflation period (1965-1982).

https://www.ssa.gov/news/en/cola/

After those tumultuous early years, the COLA settled out to an average of 2.4 percent between the years of 1984 and 2020, with several years (2010, 2011, & 2016) having no increase at all. But the fourth-highest COLA on record is in our not-too-distant past. In 2022, inflation rose again due to the effects of the COVID-19 pandemic and Russia’s war on Ukraine, and the COLA benefits rose 4.6 percent from 1.3 to 5.9 percent. Then in 2023, that fourth-highest spot was secured with an 8.7 percent raise in benefits.

So, where are we today?

Inflation has cooled since 2023, and the COLA for 2024 was reflective of that with a 5.5 percent decrease. Since then, things have stabilized around the 3 percent range. In October of last year, the Social Security Administration announced a 2.8 percent COLA for 2026 (a slight increase from 2025), bringing an estimated $56 more to beneficiaries’ checks starting this month.

Though we don’t know what the future of Social Security and its accompanying COLAs may look like, it is an important part of many people’s retirement planning and will most likely continue in some form or another. Though, as we can see from its past, adaptations (like the automatic COLAs!) may need to be made. As Social Security Commissioner Frank J. Bisignano says,

“Social Security is a promise kept, and the annual cost-of-living adjustment is one way we are working to make sure benefits reflect today’s economic realities and continue to provide a foundation of security. The cost-of-living adjustment is a vital part of how Social Security delivers on its mission.”

If you would like to see how Social Security fits into your retirement plan and help ensure inflation doesn’t derail your ideal retirement, contact us today for a complimentary review of your finances.

Sources:

https://www.ssa.gov/news/en/press/releases/2025-10-24.html

https://www.aarp.org/social-security/cola-history

https://www.ebsco.com/research-starters/history/social-security-act-1935

This material is intended for educational purposes only and is not intended to serve as the basis for any purchasing decision. The source(s) used to prepare this material is/are believed to be true, accurate and reliable, but is/are not guaranteed. This material is not endorsed or approved by the Social Security Office or any other Government Agency.

SWG 5047616-1225